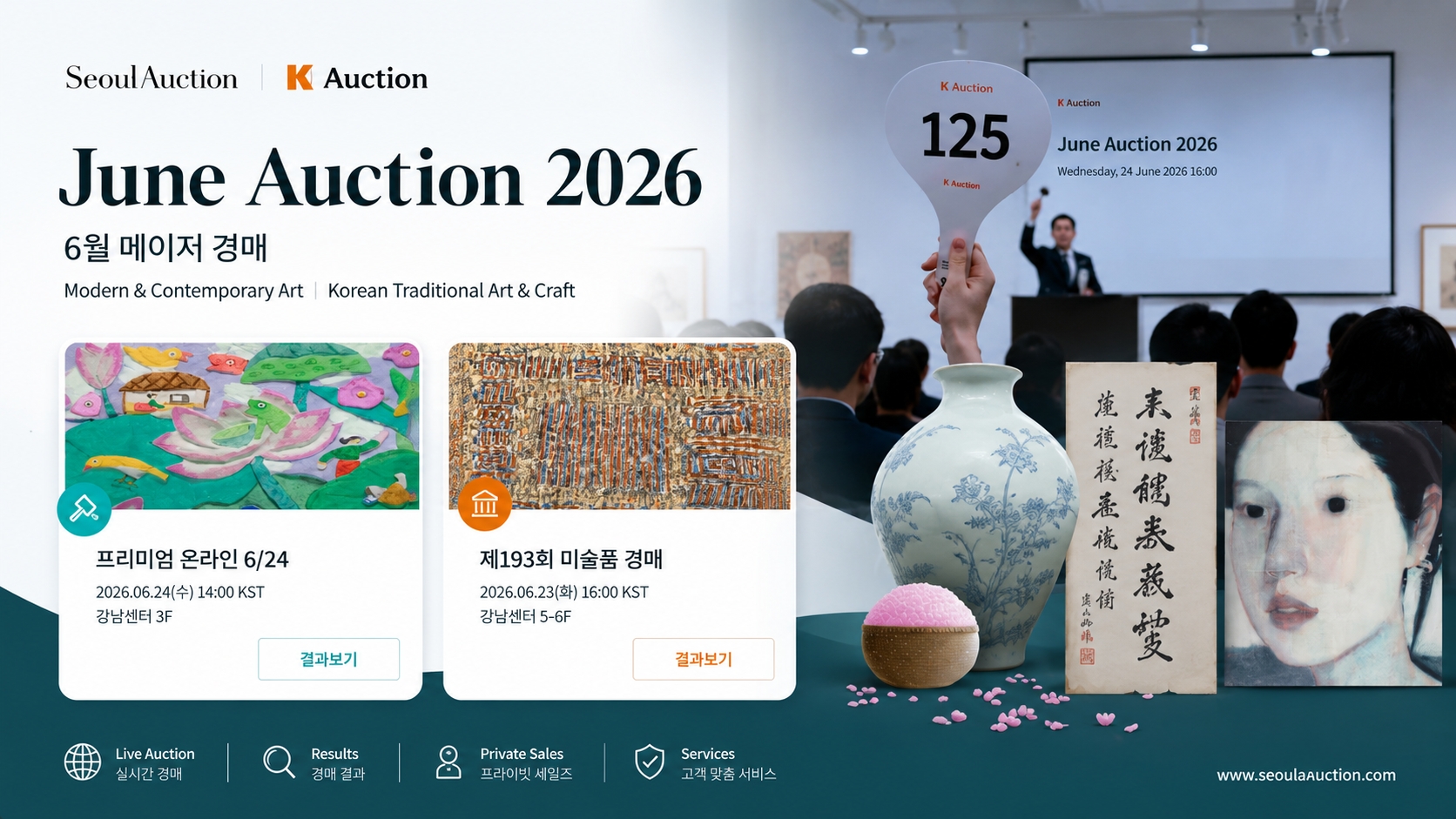

The results of

the major May auctions held by Seoul Auction and K Auction in the last week of

May 2026 show that the Korean art market is beginning to move again. However,

this movement should be understood not as a full-scale recovery, but rather as

a pattern of selective transactions that varies according to artwork category,

price range, artist recognition, and the character of the collector base.

K Auction

recorded total sales of approximately KRW 7.2321 billion (approx. USD 4.78

million) and a sell-through rate of 77.9% at its major auction held on May 27.

Of the 77 lots offered, 60 were sold. The top lot was Yayoi Kusama’s >Infinity

Nets (POWTY), which was offered with an estimate of KRW 2.1

billion–3.5 billion (approx. USD 1.39 million–2.31 million) and sold for KRW

2.1 billion (approx. USD 1.39 million).

Seoul Auction

recorded total sales of approximately KRW 5.66 billion (approx. USD 3.74

million) and a sell-through rate of 69.8% at its 192nd art auction held on May

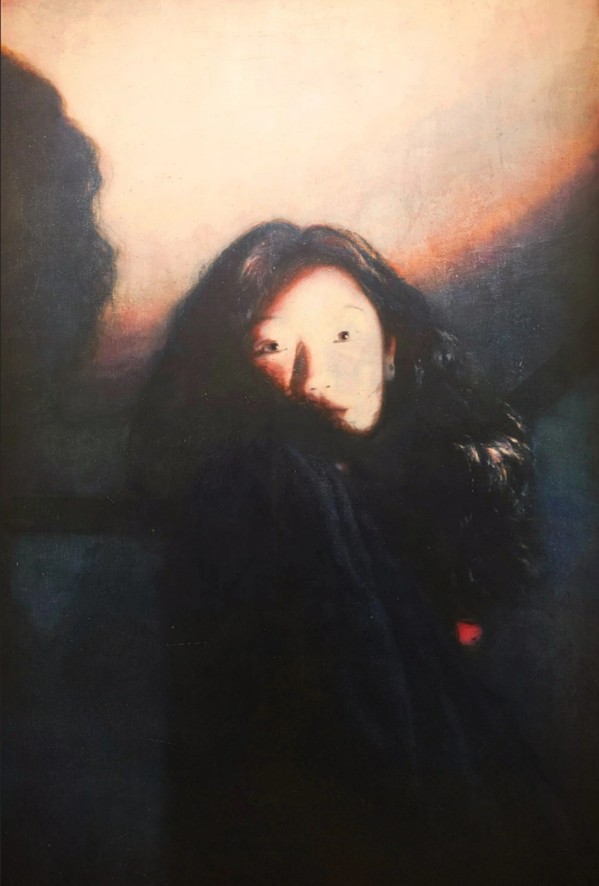

28. At Seoul Auction, Lee Ufan’s Dialogue was offered

with an estimate of KRW 700 million–1.2 billion (approx. USD 463,000–794,000)

and sold for KRW 1.04 billion (approx. USD 688,000).

Lee Ufan, Dialogue, 2018, acrylic on canvas, 130.3 × 96.8 cm. / Photo: Seoul Auction

Taken together,

the results of the two auctions show that high-priced blue-chip works continue

to form a central axis of the market, but not every high-priced work is

automatically absorbed. At the same time, strong bidding emerged around

specific works by younger artists. This is the key point of the May auctions.

The market is moving, but that movement is not broad or uniform. Rather, it

appears selectively according to the character of each work and the conditions

of its price.

K

Auction: Blue-Chip Stability and Competition for Mid- to Lower-Priced

Contemporary Works

K Auction’s

results were generally stable. Its sell-through rate approached 80%, and total

sales exceeded KRW 7 billion (approx. USD 4.63 million), marking a relatively

strong performance within the recent auction market.

Yayoi Kusama, Infinity-Net (POWTY), 2014, acrylic on canvas, 145.5 × 145.5 cm.

/ Photo: Sotheby’s

Yayoi Kusama’s Infinity

Nets (POWTY), which achieved the highest price of the sale, was

offered with an estimate of KRW 2.1 billion–3.5 billion (approx. USD 1.39

million–2.31 million) and sold at the low estimate of KRW 2.1 billion (approx.

USD 1.39 million). The fact that the work sold at the low estimate suggests

that the current market is moving less through aggressive bidding above the

estimate and more through the acceptance of proven works at realistic price

levels.

Do Ho Suh’s large-scale installation Cause & Effect. / Photo: K Auction

Do Ho Suh’s

large-scale installation Cause & Effect was

offered with an estimate of KRW 280 million–600 million (approx. USD 185,000–397,000)

and sold for KRW 360 million (approx. USD 238,000). Compared with paintings or

two-dimensional works, installation works involve more complex conditions

related to storage, installation, and resale. Therefore, the sale of this work

can be seen not simply as a transaction, but as a useful reference point for

considering how far the domestic auction market can expand its acceptance of

contemporary art.

Yoo Youngkuk, Mountain, 1988, oil on canvas, 65.1 × 90.9 cm. / Photo: K Auction

Yoo Youngkuk’s

1988 work Mountain was offered with an estimate of

KRW 400 million–800 million (approx. USD 265,000–529,000) and sold for KRW 490

million (approx. USD 324,000). This result shows that basic demand for Korean

abstract art remains in place. However, rather than indicating an aggressive

price increase, it is closer to a case in which a work by a proven artist was

absorbed by the market within an appropriate price range. The current market is

not at a stage where it accepts high prices based on the artist’s name alone.

The date of production, size, series, and realism of the estimate all operate

together.

Moonassi, Awareness, ink and acrylic on hanji, 60.6 × 72.7 cm, 2022. / Photo: K Auction

An interesting

case at this K Auction sale was Moonassi’s Awareness.

The work started at KRW 8 million (approx. USD 5,300) and sold for KRW 26

million (approx. USD 17,200) after 42 bids. What matters in this case is not

the sale price itself, but the density of bidding.

Whether this

competition resulted from participation by a broad collector base or from

repeated bidding among a small number of bidders needs to be examined

separately. Competition at auction may reflect actual demand, but it can also

function as a mechanism that publicly exposes and establishes the price of a

specific work. Therefore, this result can be read both as a sign of market

activity and as a case that requires further verification of the price

formation process.

Seoul

Auction: Bidding Concentrated on Modern and Contemporary Blue Chips and Young

Artists

Seoul Auction’s

results were somewhat more limited compared with K Auction’s. Total sales

amounted to approximately KRW 5.66 billion (approx. USD 3.74 million), with a

sell-through rate of 69.8%. The colored manuscript version of Daedongyeojido,

which had been mentioned as a highly anticipated lot, was offered at a low

estimate of KRW 2 billion (approx. USD 1.32 million), but failed to sell.

The colored

manuscript version of Daedongyeojido is a special

item that differs from ordinary paintings or contemporary artworks. As a

historical document of cultural-property-level significance, it clearly

possesses scholarly value and rarity. However, the collector base capable of

purchasing such an item at auction is limited.

Several

conditions must align for a transaction to take place, including storage,

research purpose, collecting purpose, the possibility of institutional

acquisition, and price acceptability. Therefore, this failure to sell should be

understood not as a sign of weakness in the entire antique art market, but

rather as the result of a mismatch between the work’s price and buyer

conditions at this particular auction.

Lee Mokha’s Chroma Key Blue. / 사진: Seoul Auction

The more

noteworthy point in Seoul Auction’s results was the competition for a young

artist. Lee Mokha’s Chroma Key Blue was offered with

an estimate of KRW 100 million–150 million (approx. USD 66,000–99,000) and sold

for KRW 350 million (approx. USD 231,000). This was a case that showed a level

of price acceptance beyond simple interest. At the same time, it also shows the

need to examine what supports such a price when a young artist’s work enters a

high-price range within a short period of time.

Moonassi

and Lee Mokha: Similar Competition, Different Price Structures

The results for

Moonassi and Lee Mokha both show market interest in young artists. However, the

market significance of the two cases differs.

Moonassi’s Awareness

started at KRW 8 million (approx. USD 5,300) and sold for KRW 26 million

(approx. USD 17,200). This was a case in which multiple bidders were drawn to a

relatively accessible price range. In this case, the key point is not the

height of the sale price, but the breadth of bidding participation. If

competition emerges from a low starting price and the price rises through

repeated bidding, this may be seen as a case that demonstrates liquidity in the

mid- to lower-priced contemporary art market.

By contrast, Lee

Mokha’s Chroma Key Blue was offered with an estimate

of KRW 100 million–150 million (approx. USD 66,000–99,000) and sold for KRW 350

million (approx. USD 231,000). In this case, the key issue is not price

accessibility but the market’s willingness to accept a high price. For a work

by a young artist to trade at this level, simple preference for the image is

not enough as an explanation. It is likely that several factors operated

together: the artist’s recent market attention, the representative quality of

the work, exhibition history, gallery price management, expectations of future

price appreciation, and symbolic value within contemporary art.

However, this is

precisely where careful interpretation is required. The fact that a work by a

young artist greatly exceeds its estimate or attracts many bids does not

automatically prove that the market is healthy. Auction prices may reflect

actual demand, but at times they also function to publicly establish a price

and signal it to the market. Especially when auction prices rise before an

artist’s institutional validation or critical foundation has been sufficiently

formed, the price may reflect market expectations brought forward rather than

market trust.

Therefore, the

cases of Moonassi and Lee Mokha show vitality in the young artist market while

also requiring closer examination of the structure of price formation. What

matters is not the sale price itself, but the conditions under which that price

was created. The breadth of actual bidders, the relationship with primary

market prices, whether similar works are repeatedly offered, post-sale payment

and resale records, and the artist’s exhibition and critical foundation must

all be confirmed together.

Criteria

for Evaluating Auction Results for Young Artists

To properly

evaluate auction results for young artists, at least six criteria need to be

considered together.

First,

the gap between primary market prices and auction sale prices.

It is necessary

to examine the extent of the difference between the recent prices formed by

galleries and the prices achieved at auction. If the gap is large, there must

be grounds that can explain the increase, such as exhibitions, institutional

acquisitions, critical evaluation, overseas exposure, or expanded demand. If

auction prices move too far ahead of primary market prices, questions may arise

about the stability of price formation.

Second,

the frequency of consignments and repeated sales.

If works by a

young artist appear repeatedly at multiple auctions within a short period of

time, this should be watched carefully. In a healthy market, good works tend to

be absorbed by collectors and held for a certain period. By contrast, if

similar works are quickly and repeatedly consigned, this may indicate that

selling pressure is stronger than collecting demand, or that a tendency to

expose prices through auction is at work.

Third,

the quality of bidding.

A high number of

bids does not necessarily mean that the demand base is broad. What matters is

how many actual bidders participated, whether bidding was concentrated only at

lower price levels, and whether multiple competitors remained in the final

high-price range. Even in a case of more than 40 bids, it is possible that the

competition was created by a small number of bidders repeatedly bidding in

small increments. Therefore, the number of bids is only a reference indicator;

it does not in itself prove the health of the market.

Fourth,

actual payment after the sale and resale records.

The fact that a

work was sold at auction does not by itself confirm the price. It is necessary

to verify whether payment was actually completed, whether similar works later

trade again at a comparable price level, and whether the price is maintained in

subsequent auctions.

Fifth,

the breadth of actors supporting the price.

For the price of

a young artist’s work to be formed in a healthy way, it must not depend only on

a specific auction house or a specific collector group. Galleries, collectors,

institutions, criticism, and exhibition history must operate together. If the

price is formed only among a narrow group of market participants, the breadth

of demand may be limited. By contrast, if institutional exhibitions, major

collections, critical discussion, and international exposure provide support

together, the persuasiveness of the price increases.

Sixth,

the representative quality and artistic quality of the work.

Even in the case

of a young artist, a high-price transaction becomes more persuasive when the

work is representative, clearly shows the artist’s core language, belongs to an

important period, or has an exhibition history. By contrast, if a secondary

work or a work distant from the artist’s core language rises excessively, the

basis for the price becomes weak. In the young artist market, the

representative quality of the work itself is especially important, more than

the artist’s name alone.

Review

of the May Auction Results: Price Formation and Market Trust

The May major

auction results of Seoul Auction and K Auction confirmed stable demand in the

blue-chip market, selective competition in the young artist market, and limited

transaction conditions for special items.

In particular,

high-priced sales and multiple bids for young artists can be signs of market

vitality, but they do not by themselves prove price stability. For prices

formed at auction to become sustainable market prices, they must be supported

by the representative quality of the work, the artist’s exhibition history,

critical evaluation, primary market price management, and the breadth of the

actual collector base.

Ultimately, the

key point to be confirmed from the May auctions is not whether prices rose, but

whether those prices are persuasive. A good market is not one that produces

many high prices, but one that can explain why those prices are possible. For

the Korean art market to grow in a sustainable direction, auction results must

not be consumed merely as indicators of excitement. The process through which

prices are formed, and the structure that supports those prices, must be read

more rigorously.