Recently, major

media outlets including The New York Times, the

international contemporary art platform Ocula, and ARTnews

have extensively reported on the large-scale restructuring of Pace Gallery, one

of the world’s leading mega-galleries.

Pace Gallery headquarters and international locations / Photo: Edited from Pace Gallery website

In particular,

remarks by Pace CEO Marc Glimcher describing the current gallery model as not

merely “broken” but effectively “unfixable” have sent ripples throughout the

global art world.

Marc Glimcher, CEO of Pace Gallery / Photo: JUSTJARED

Pace is

reportedly reducing its roster by approximately 50 artists and cutting around

50 staff positions. This is not simply a matter of downsizing or cost

reduction. Rather, it can be understood as a fundamental reassessment of the

mega-gallery model that has dominated the global art market for decades.

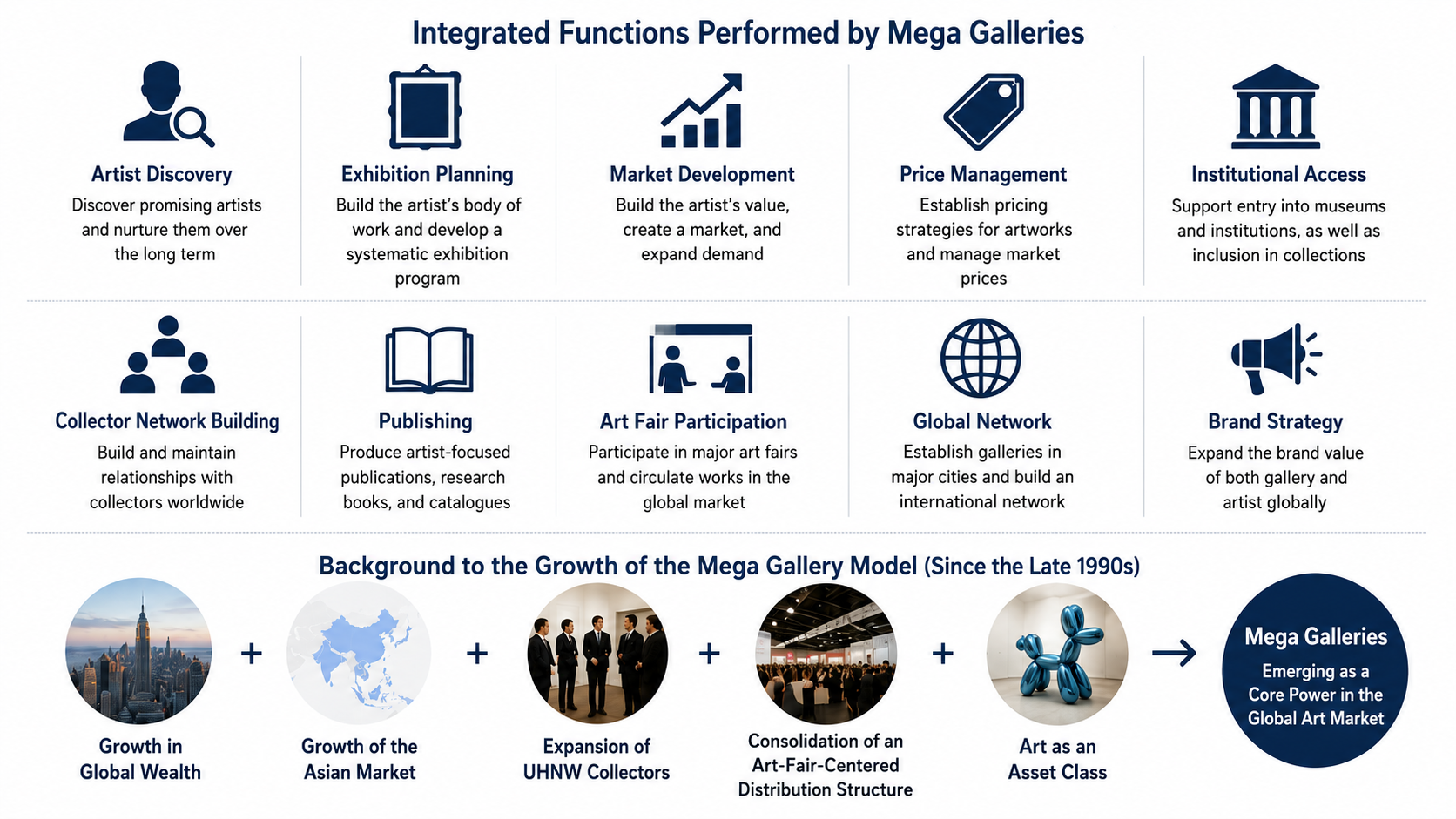

The

Rise of the Mega-Gallery Model

The mega-gallery

model does not simply refer to a large gallery. It describes a structure in

which galleries evolved beyond individual exhibition spaces into global,

corporate-scale art distribution systems.

Galleries such as

Pace, Gagosian, Hauser & Wirth, and David Zwirner established locations

across major international cities including New York, London, Paris, Hong Kong,

Seoul, and Los Angeles, representing dozens or even hundreds of artists and

artist estates while building extensive global networks.

These

organizations developed into complex systems that extend far beyond selling

artworks. They became involved in artist discovery, exhibition programming,

market development, price management, museum placement, collector-network

cultivation, publishing, art fair participation, and global branding

strategies.

Since the late

1990s, the simultaneous growth of global wealth, the expansion of Asian

markets, the rise of ultra-high-net-worth collectors, the establishment of

art-fair-driven distribution channels, and the financialization of art have

positioned mega-galleries at the center of power within the global art market.

Expansion

became synonymous with success.

More artists,

more locations, more art fairs, more projects, and more revenue came to be

regarded as the primary indicators of growth.

Figure 1. The Mega-Gallery Business Model

The

Structural Limits of the Growth Model

Yet while the

mega-gallery model proved highly effective during periods of growth, it became

increasingly burdensome during periods of stagnation.

The fixed costs

associated with maintaining global locations, large exhibition spaces,

shipping, insurance, staffing, and participation in international art fairs

continued to rise. Such expenses were manageable when the market was expanding,

but as sales activity began to slow, they quickly became liabilities.

The

growth in artist rosters created additional challenges.

When a gallery

represents more than one hundred artists, it becomes increasingly difficult to

provide each artist with adequate exhibition opportunities, institutional

introductions, critical support, and market development. Resources inevitably

become concentrated around a small group of blue-chip artists, while many

others remain represented largely in name.

The

role of the gallery also began to change.

Traditionally,

galleries were responsible for nurturing and developing an artist’s practice

over the long term. As galleries expanded, however, they increasingly resembled

portfolio-management systems rather than spaces dedicated to cultivating

artists and supporting artistic development.

The

international distribution system centered on art fairs further accelerated

this shift.

Continuous

participation in major fairs requires a constant supply of new works and new

sales strategies. As a result, both artists and galleries became increasingly

responsive to short-term market performance and immediate sales results rather

than long-term value formation.

The

Time of Art and the Time of Capital

This development

reveals a more fundamental issue.

It represents a

collision between the time of art and the time of capital.

The

time of art is slow.

It can take

decades for an artist to develop a distinct visual language, establish a body

of work, undergo critical evaluation, and secure a meaningful position within

art history. Artistic value emerges gradually through exhibitions, research,

criticism, collecting, and continual reassessment.

The

time of capital, by contrast, is fast.

It demands more

transactions, faster turnover, higher growth rates, and more immediate returns.

Over the past

several decades, the global art market has increasingly operated according to

the logic of capital. More artists, more exhibitions, more art fairs, and

faster price appreciation became the dominant objectives.

Yet

while prices can be created quickly, value cannot.

The Pace case can

therefore be interpreted as a symbolic moment in which the time of art can no

longer keep pace with the accelerating demands of capital.

Figure 2. The Time of Art vs. The Time of Capital

The

Market Is Not Collapsing—It Is Being Reconfigured

It is

insufficient to interpret this event simply as evidence of market decline.

A phrase

increasingly heard in international art-market discussions is: “The art

market isn’t collapsing. It’s separating.”

In other words,

the market is not disappearing—it is becoming increasingly divided.

Blue-chip works

and the ultra-high-end segment continue to perform strongly. Meanwhile, the

middle market and the market for many mid-career artists are weakening, placing

growing pressure on galleries operating within those segments.

The

issue is therefore not the disappearance of the market, but a transformation of

its structure.

Pace’s

restructuring demonstrates that these pressures have now reached even the level

of the mega-galleries themselves.

The

Post–Mega-Gallery Era

The significance

of this event extends beyond Pace’s restructuring alone.

It may signal

that the expansion-driven model that has dominated the global art market for

the past twenty to thirty years is no longer capable of defining the future.

In place of a

model built on representing ever-larger numbers of artists, greater importance

is now being placed on supporting a smaller number of artists with greater

depth and commitment.

Trust is becoming

more important than volume.

Documentation,

criticism, research, and archives are becoming more important than marketing

alone.

The global art

market may be entering a transition from an era of growth to an era of

maturity, and from an era of expansion to an era of accumulation.

What

Korean Contemporary Art Should Pay Attention To

This event also

offers important implications for the Korean art world.

The challenge

facing Korean contemporary art is not one of excessive expansion. Rather, it is

the opposite. The infrastructure necessary to continuously introduce, document,

evaluate, and connect Korean artists to the international art world remains

insufficiently developed.

For many years,

the globalization of Korean art has been understood primarily in terms of

visibility—participation in overseas exhibitions, international art fairs, and

connections with foreign galleries and collectors. Yet visibility alone is not

enough for an artist to secure a lasting position within the international art

ecosystem.

Artwork images,

artist biographies, exhibition histories, collection records, critical essays,

interviews, artwork descriptions, provenance documentation, media coverage, and

high-quality English-language materials must be systematically accumulated and maintained.

If the global art

market is moving from an era of growth and expansion into one of maturity and

restructuring, then the task facing Korean contemporary art becomes

increasingly clear. The goal is not to replicate the external form of the

mega-gallery model, but to build the foundations through which Korean artists

can be understood, evaluated, and trusted internationally.

Ultimately,

the essence of globalization is not scale but credibility.

No matter how

strong the artists or how significant the artworks may be, without systems

capable of documenting, interpreting, translating, and connecting them, it is

difficult to secure a sustained position within the global art world.

For this reason,

the most urgent task facing Korean contemporary art today is not outward

expansion, but the careful construction of reliable information systems,

documentation practices, critical discourse, and archival infrastructure

capable of earning international trust.

Jay Jongho Kim graduated from the Department of Art Theory at Hongik University and earned his master's degree in Art Planning from the same university. From 1996 to 2006, he worked as a curator at Gallery Seomi, planning director at CAIS Gallery, head of the curatorial research team at Art Center Nabi, director at Gallery Hyundai, and curator at Gana New York.

From 2008 to 2017, he served as the executive director of Doosan Gallery Seoul & New York and Doosan Residency New York, introducing Korean contemporary artists to the local scene in New York. After returning to Korea in 2017, he worked as an art consultant, conducting art education, collection consulting, and various art projects.

In 2021, he founded A Project Company and is currently running the platforms K-ARTNOW.COM and K-ARTIST.COM, which aim to promote Korean contemporary art on the global stage.