One of the most significant stories in the

global art world recently has been Pace Gallery’s large-scale staff reductions

and restructuring of its artist roster. Across the international art community,

the news was widely interpreted as a sign of crisis within the mega-gallery

model.

Before the implications of that development

had fully settled, another major announcement emerged: the merger of Artnet and

Artsy.

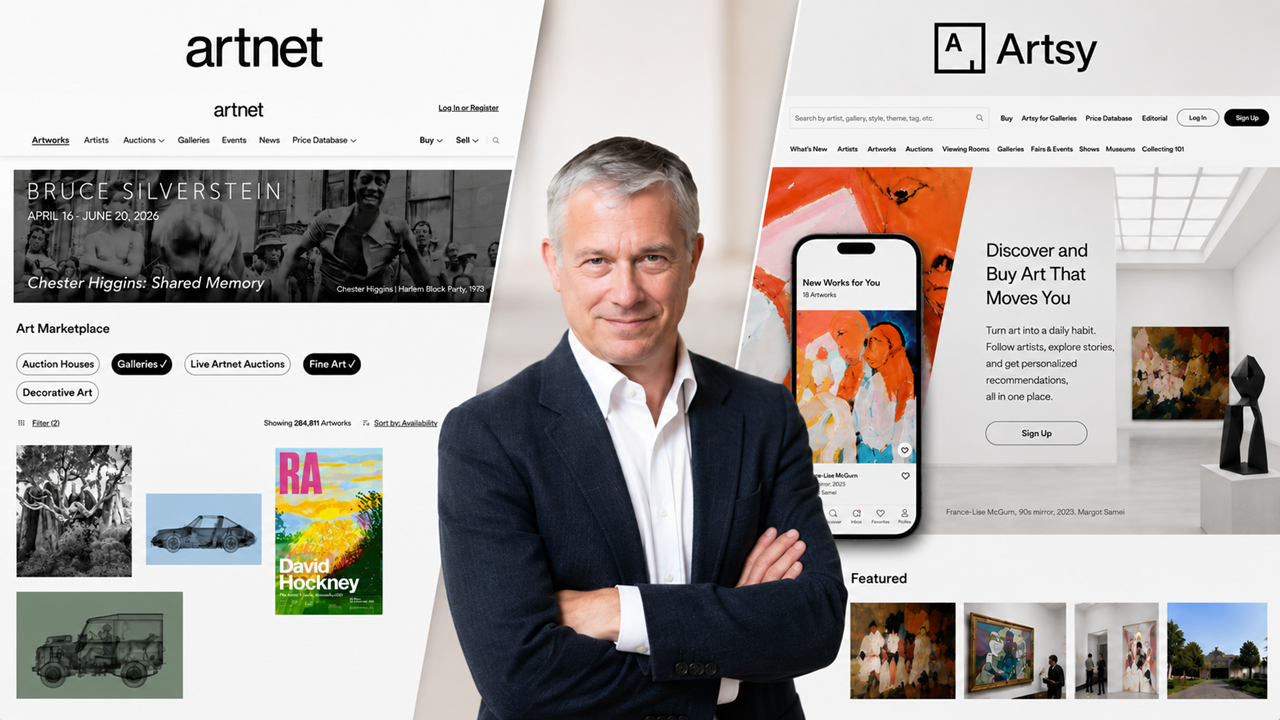

Artsy.net / Photo: Homepage screen capture

Artnet.com / Photo: Homepage screen capture

Artnet is one of the world’s leading

platforms for auction data and secondary-market information. Artsy operates a

global online platform connecting collectors, galleries, and artists through

artwork discovery and sales. Together, the two companies appear poised to

create a massive art platform where users can discover artists, search

artworks, access pricing information, and conduct transactions within a single

ecosystem.

Andrew Wolff. / Photo: Beowolff

Their new owner, Andrew Wolff, has

articulated an ambitious vision: combining Artnet’s extensive auction database

with Artsy’s gallery network to build what he calls a “Bloomberg for Art.”

At first glance, the idea sounds

compelling. Data, market intelligence, gallery networks, online transactions,

and analytics would be integrated into a single platform. It appears to be a

thoroughly contemporary business model.

Yet the central question is not whether the

project can be executed. The real question is whether it can succeed.

The Collision Between Platform

Capitalism and Fine Art

The fundamental problem with the Artnet–Artsy

merger is that it applies the logic of digital platform capitalism directly to

the art market.

Amazon grew because products can be

manufactured and sold endlessly. Netflix expanded because content can be

reproduced infinitely. Google became a global platform because both users and

searchable information can continue growing without practical limits.

The foundation of platform capitalism is

scalability. As users increase, value increases. As transactions multiply,

revenue grows. As data accumulates, market dominance strengthens.

Fine art, however, operates according to

entirely different principles.

Fine Art Cannot Be Infinitely

Produced

Great artworks are not produced endlessly.

Great artists do not emerge endlessly. The most important works of any artist

are always limited, and it is precisely this scarcity that generates value.

If artworks could be produced infinitely,

they would cease to function as fine art in the traditional sense. Fine art is

fundamentally incompatible with the logic of mass production, cost reduction,

infinite replication, and scalable growth.

The art market is not a market of

reproduction. It is a market of scarcity.

More users on a platform do not create more

masterpieces. More data does not produce more important artworks. More

transaction tools do not transform the art market into Amazon.

This is where the core contradiction of the

Artnet–Artsy project emerges. They seek growth through the logic of platforms. Yet

art is not an industry capable of infinite platform-driven growth.

Amazon.com / Photo: Homepage screen capture

Artworks Are Not Consumer

Necessities

Art is not a necessity. Nor is it an

ordinary consumer product.

Buying a book on Amazon and purchasing an

artwork worth hundreds of thousands or millions of dollars are fundamentally

different activities.

Most people never buy art. Even collectors

purchase only a limited number of works. The more significant an artwork

becomes, the higher its price and the lower its accessibility.

Artworks involve transportation, storage,

installation, insurance, customs regulations, and international logistics. More

importantly, they require direct experience.

Art can be represented through images, but

it cannot be fully replaced by images. Important exhibitions must still be

experienced in person, and major works reveal their full significance only

within physical space.

This is one reason why the art market

cannot easily evolve into a large-scale consumer market.

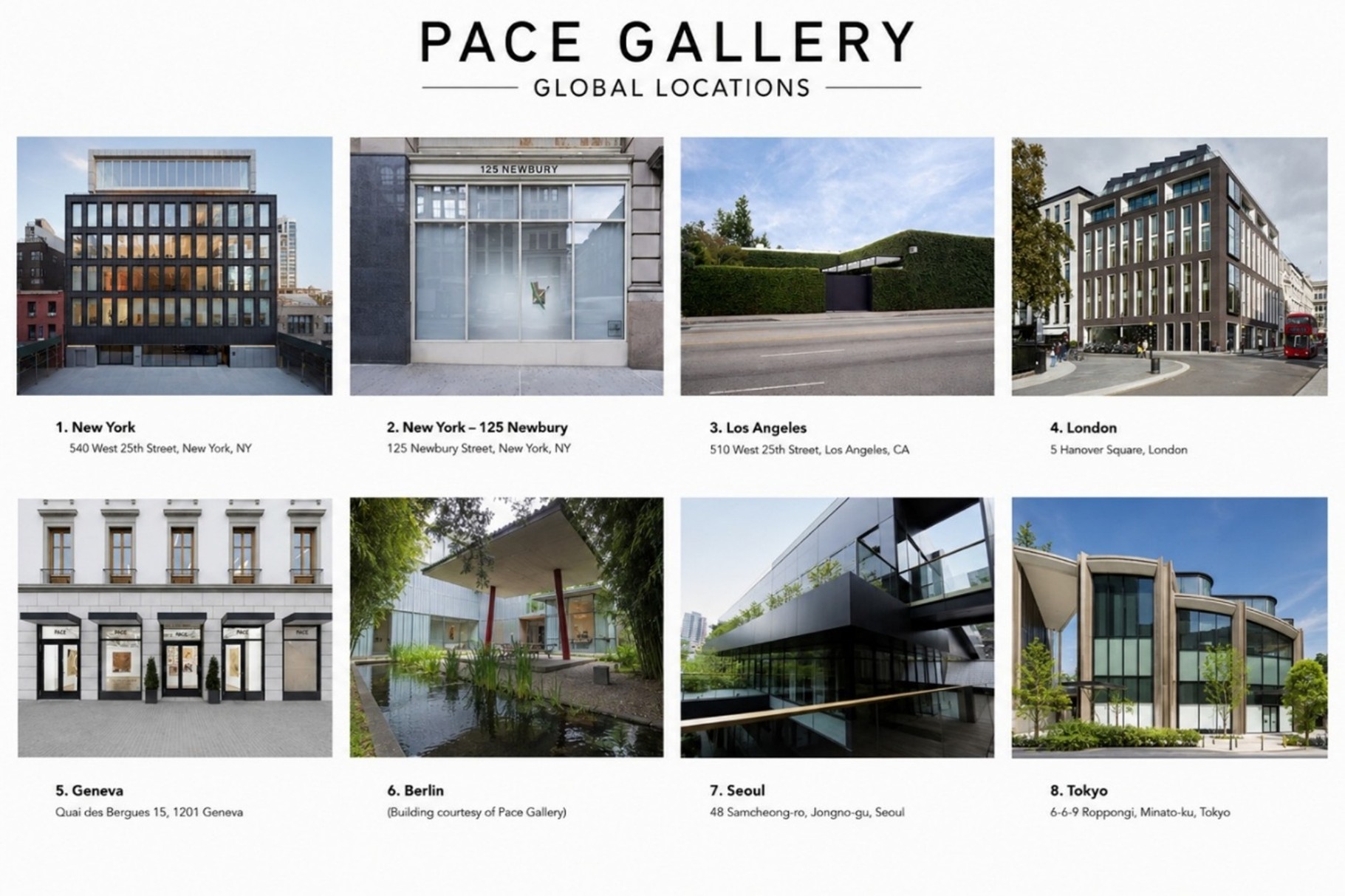

Pace Gallery headquarters and international locations / Photo: Edited from Pace Gallery website

What the Pace Gallery Case

Reveals

The recent changes at Pace Gallery make

this reality even more visible.

Many observers interpret the gallery’s

restructuring as a consequence of market contraction or management

difficulties. Yet from a broader perspective, it may represent something more

fundamental: the limits of applying endless-growth logic to art.

Over the past two decades, mega-galleries

pursued continual expansion. More locations. More artists. More employees. More

art fairs. More transactions.

But art is not an industry built for

limitless growth. The number of truly important artworks remains limited. The

number of exceptional artists remains limited as well. Eventually, the growth

demanded by capital collides with the natural pace of artistic production.

The Pace Gallery story is therefore not

simply a story of market failure. It is a reminder that art cannot be

transformed indefinitely into a conventional growth industry.

The Impossible Project of

Artnet and Artsy

What, then, does the Artnet–Artsy merger

represent?

Rather than signaling the future of digital

platforms, it may ultimately reveal the limits that platform capitalism

encounters when it enters the field of art.

The vision of a “Bloomberg for Art” is

certainly intriguing. But financial markets and art markets operate according

to different principles.

Financial markets are driven primarily by

information and numbers. Art markets are driven by artworks, experience,

interpretation, and meaning. The price of art can be measured through data. The

value of art cannot.

Artnet and Artsy seek to transform art into

a unified system of data, transactions, and information. Yet the essence of art

exists beyond data.

It resides in materiality, scarcity,

experience, historical context, and the endless possibility of interpretation.

Data Matters, But It Cannot

Replace Art

Data is important. Archives are important. Market

transparency is important. The art world undoubtedly needs better information

and more reliable data.

But data remains infrastructure. It is not

art itself.

Good data does not create great artworks.

Large user numbers do not create great artists. Platform scale does not

guarantee artistic value.

The essence of art remains in the work

itself and in the experiences and interpretations it generates.

The Artnet–Artsy merger may create new

opportunities in the short term. Whether it can produce the kind of scale and

profitability achieved by major technology platforms, however, is an entirely

different question.

More likely, it may become a case study

illustrating the structural limits that emerge whenever art encounters the

logic of capital.

What the Korean Art World

Should Learn

This issue carries important implications

for Korea as well.

The goal should not be to imitate platforms

such as Artnet and Artsy. Instead, it is necessary to understand the structural

limitations of the capitalization and platformization currently unfolding in

the Western art world.

The globalization of Korean art will not be

achieved through more art fairs, more biennials, or more exhibitions of

internationally famous artists.

What is needed are accurate archives,

serious criticism, internationally accessible language, reliable documentation,

and sustainable market structures.

Rather than following the path already laid

out by the Western art world, Korean contemporary art should use this moment of

global restructuring to design new systems that are better aligned with the

nature of art itself.

Art Is Not Money, Money Is Not

Art

Art can meet capital. Art can be traded

within markets. Art can reach broader audiences through data and digital

platforms.

But art can never become capital itself. Art

may be a commodity, but it is never merely a commodity. It exists within

markets, yet it can never be fully reduced to market logic.

This is the fundamental nature of fine art.

Art is not money. Money is not art.

"Art is art. Money is money. Art is not money. Money is not art."

Jay Jongho Kim graduated from the Department of Art Theory at Hongik University and earned his master's degree in Art Planning from the same university. From 1996 to 2006, he worked as a curator at Gallery Seomi, planning director at CAIS Gallery, head of the curatorial research team at Art Center Nabi, director at Gallery Hyundai, and curator at Gana New York.

From 2008 to 2017, he served as the executive director of Doosan Gallery Seoul & New York and Doosan Residency New York, introducing Korean contemporary artists to the local scene in New York. After returning to Korea in 2017, he worked as an art consultant, conducting art education, collection consulting, and various art projects.

In 2021, he founded A Project Company and is currently running the platforms K-ARTNOW.COM and K-ARTIST.COM, which aim to promote Korean contemporary art on the global stage.